Many people are pondering their course of action given the recent turmoil in geopolitical affairs where Russia has invaded Ukraine and the volatility of the stock market.

Which makes the most sense to you? Getting out of the stock market because there has been volatility, or staying the course and letting the market settle down before making emotional decisions that could be detrimental to your financial health?

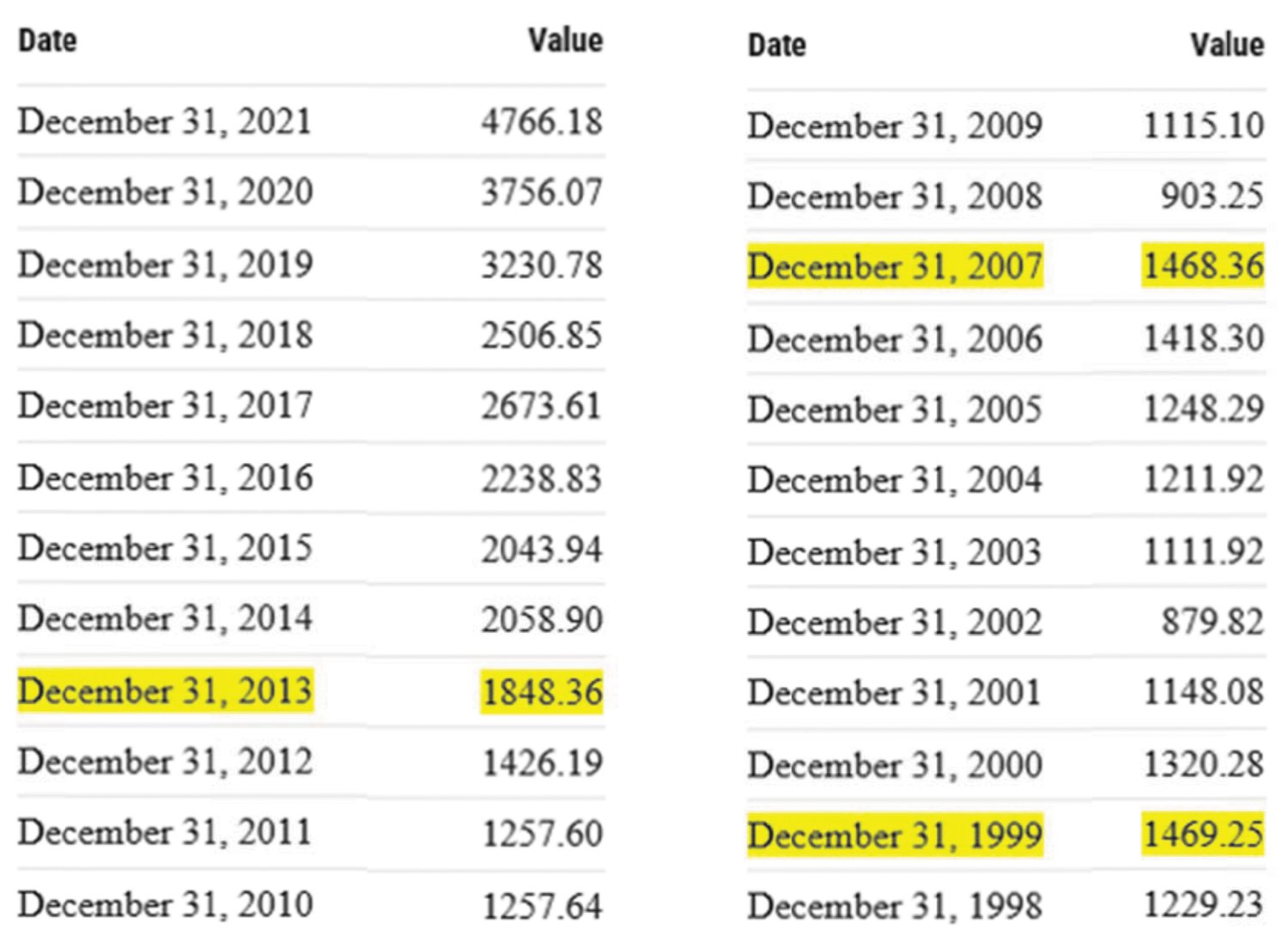

Well, let’s take a walk down the memory lane of stock market gyrations. If we go back to 2000, the first of a 3-year decline in the stock market, that lost approximately 10% of value. Followed by 2001 with a 13% loss, followed by 2003 with a 23% loss. Those were three tough years to live through, especially if you were withdrawing cash to pay your bills in retirement. Which, we don’t recommend. (https://ycharts.com/indicators/sp_500_annual, n.d.)

That 3-year loss of value was disconcerting, to say the least. However, if you bailed out of the market at the end of that third year, you would have missed the massive recovery that unfolded over the next four years.

Sadly, there was yet another period of large declines in the market that started in the fourth quarter of 2007 and ended in the “trough” as it is called (the bottom of a market decline before the market starts recovering) on March 6 of 2009. The S&P 500, at its low point, was 666.80, which again was a rough ride. The market finally recovered in 2013 from its high point in 2007.

At the end of 2021, the S&P 500 was listed as 4,766.18 from the low of 666.80. That is an increase of over 700% in 12 years! So, no surprise that the market is slowing down a bit. (https://ycharts.com/indicators/sp_500_annual, n.d.)(See the chart below)

What this history lesson teaches us is that it is far more important to have time IN the market, not TIMING the market. The typical advice is to stay the course and let the market forces trim some of this hyper-growth to position for future growth.

We call this type of market gyration the “adult” roller coaster, and we prefer to reduce the level of risk within our clients’ portfolios. We prefer to put them on the “kiddie” roller coaster of risk. Our bias is to help reduce risk.

Let’s look at a simple example, not saying this is right for everyone, it just makes the math easy here. If you were to put one half of your portfolio in the stock market and the other half in a protected position, that cannot lose value when the market goes down, here is an example of what would happen. Let’s say the stock market is down 10%, but your portfolio is down 8%. Well, if one half of your money is down 8% and the other half isn’t down at all, then you are down 4% on your entire portfolio. Is a 4% downturn in value too much for you? If it is, simply put more money into protected positions. Ultimately, the amount that you want protected is up to you, after all, it is your money!

In our opinion, this type of strategy allows for half the money to be in the market for long-term growth while protecting the other half against market losses. We refer to this strategy as the “kiddie” roller coaster as we have a bias against too much stock market risk. https://ycharts.com/indicators/sp_500_annual

https://ycharts.com/indicators/sp_500_annual

Please note, it is not possible to invest directly into the S&P 500® Index; this measure is provided solely as a gauge of overall market performance. Standard & Poor’s: “Standard & Poor’s®,” “S&P®,” and “S&P 500®” are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”). The historical performance of the S&P 500 is not intended as an indication of its future performance and is not guaranteed. This chart is not intended to provide investment, tax or legal advice. Be sure to consult a qualified professional about your individual situation. This chart does not take into account investment fees, so actual results may be different than depicted above. Hypothetical examples are provided for illustrative purposes only; it does not represent a real-life scenario and should not be construed as advice designed to meet the particular needs of an individual’s situation. Investing involves risk, including the potential loss of principal. Any references to protection benefits, safety, security, lifetime income generally refer to fixed insurance products, never securities or investment products. Insurance and annuity product guarantees are backed by the financial strength and claims-paying ability of the issuing insurance company. Massey & Associates, Inc is an independent financial services firm that utilizes a variety of investment and insurance products. Investment advisory services offered only by duly registered individuals through AE Wealth Management, LLC (AEWM). AEWM and Massey & Associates, Inc are not affiliated companies. Neither the firm nor its agents or representatives may give tax or legal advice. Individuals should consult with a qualified professional for guidance before making any purchasing decisions. 1270612 – 03/22

Comments

No comments on this item Please log in to comment by clicking here